Explore aerospace inventory overhang as resilience shifts toward ecosystem coordination, visibility, and effective redeployment.

The aerospace sector faced supply chain disruption, capacity shortages, and delivery delays. Yet one of the most consequential aftereffects remains largely unspoken: inventory.

Across OEMs, tier-1 suppliers, deeper tiers, and MROs, inventory has been accumulating steadily, raw materials procured early to lock in pricing and secure lead times, work-in-progress frozen by engineering changes, finished parts stranded by configuration shifts and spares stocked aggressively to prevent Aircraft-on-Ground events.

While each decision made sense in isolation, collectively they have created an inventory overhang that now distorts cash flow, magnifies operational risk, and strains the financial resilience of aerospace suppliers.

This is no longer merely an operational nuisance. It has become a strategic imperative.

Insurance That Accumulated into Misalignment

When lead times stretched and supplier reliability wavered, inventory emerged as the most dependable hedge against uncertainty. Procurement teams pull demand forward, secured long-lead materials, and built buffers to protect programs from disruption. In aerospace where a single missing component can ground a multi-million-dollar assembly line his behavior was entirely rational.

The challenge lies in what follows: insurance accumulation.

Unlike other industries, aerospace inventory does not unwind readily. Certification requirements, decades-long lifecycle obligations, and program-specific configurations keep inventory locked in place well beyond the original risk horizon. What begins as operational resilience gradually transitions into structural rigidity.

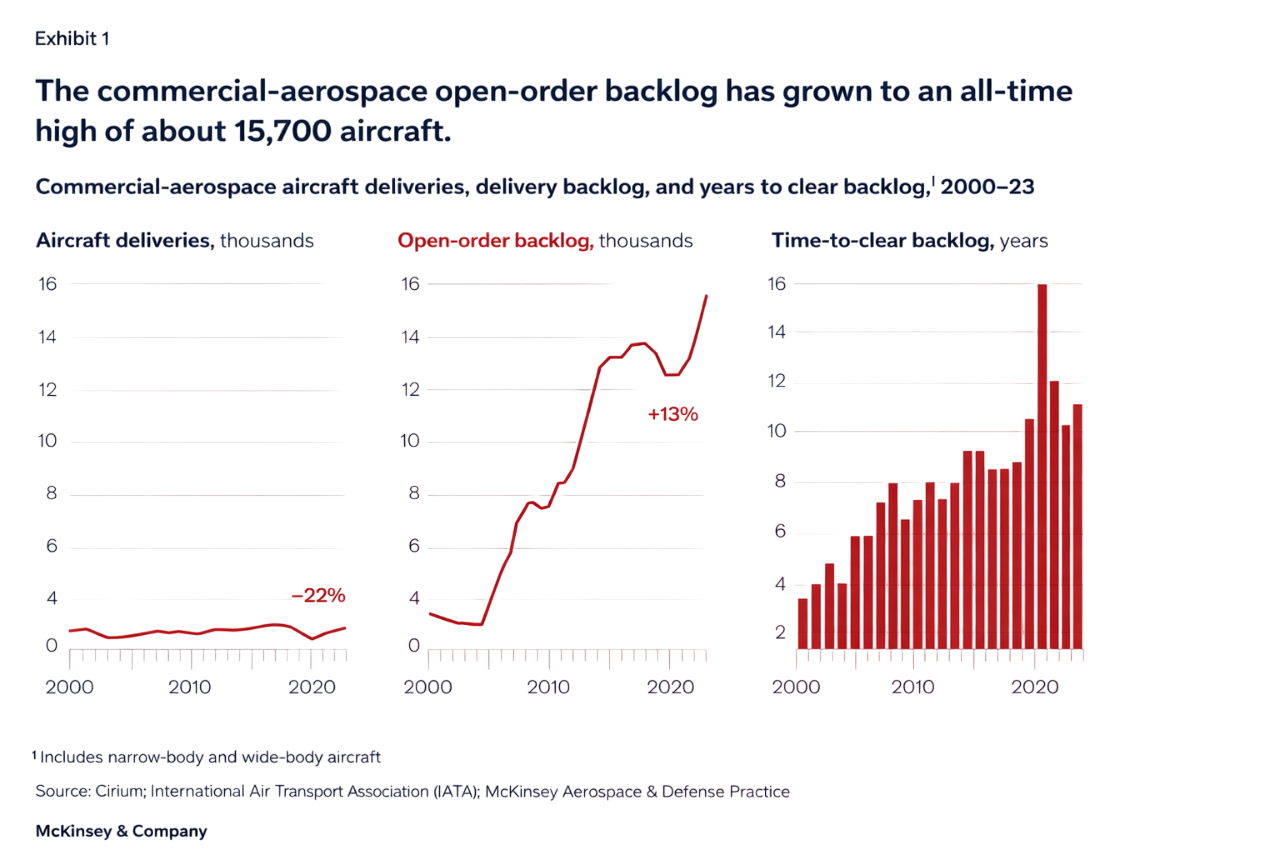

Aerospace does not suffer from weak demand. Order backlogs across commercial, defense, and aftermarket segments remain historically strong, yet shortages and excess coexist. Inventory exists, but not in the right configuration, not at the right tier, not in the right geography, and often invisible to the organization that needs it most.

Source: Addressing commercial-aerospace supply chain

This is not a forecasting failure but system‑level alignment failure. Research by McKinsey & Company shows that while visibility into tier‑1 suppliers is generally reasonable, it deteriorates sharply beyond the first tier. Tier‑2 and tier‑3 suppliers, where mismatches and bottlenecks concentrate remain opaque. The result: duplicated buffers, parallel over‑purchasing, and capital trapped in silos.

Engineering Change: The Silent Multiplier of Inventory Risk

One of the most underestimated drivers of inventory accumulation is engineering change.

Engineering now advances earlier in the lifecycle and closer to production, with design and configuration decisions running in parallel with procurement. It can pivot in weeks while certified aerospace inventory may take months to adjust. The result is material procured correctly at the time but misaligned as designs evolve.

This dynamic intensifies as aerospace engineering scales globally, including in India, where earlier procurement commitments amplify downstream exposure to OEM-level changes.

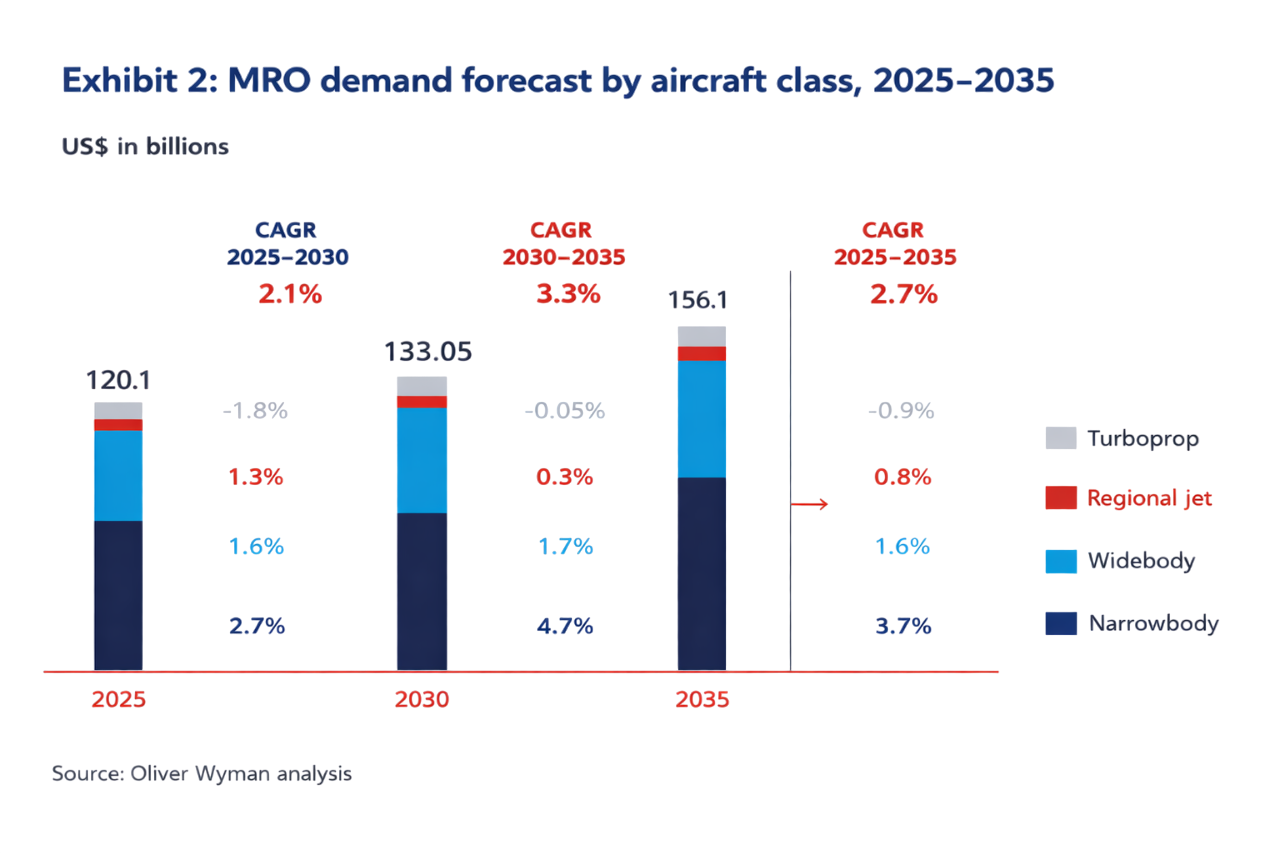

At the same time, constrained MRO capacity converts available parts into idle inventory, as components wait for shop slots highlighted by IATA and Oliver Wyman. This is not an execution failure but a structural mismatch between engineering speed, maintenance capacity, and inventory adaptability.

Source: Global Fleet And MRO Market Forecast

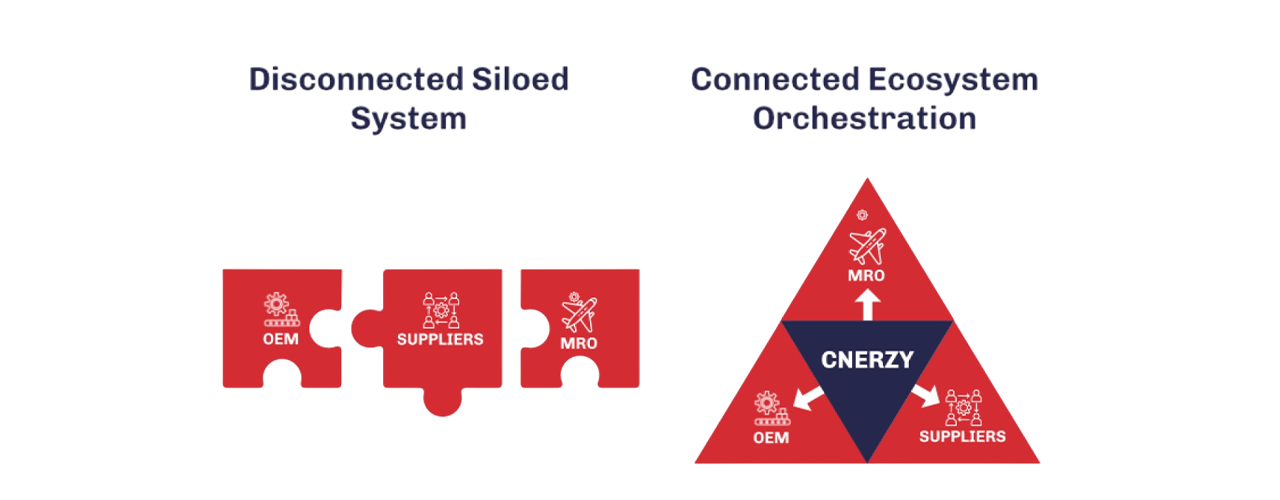

Inventory Overhang an Ecosystem Problem

Traditional inventory optimization assumes enterprise-level control. Certification slows redeployment. Multi-tier dependencies obscure inventory location. Long lifecycle obligations extend decision impact. Risk aversion delays release of precautionary stock.

Most critically, inventory, demand, engineering decisions, and maintenance capacity sit across independent enterprises.

- OEMs cannot see supplier access.

- Suppliers cannot see downstream urgency.

- MROs cannot see upstream availability.

Industry research increasingly points to multi-enterprise orchestration and not linear optimization, as the next phase of supply-chain evolution. IDC highlights ecosystem-based coordination, while Gartner underscores connected, cross-enterprise resilience in regulated industries.

For aerospace, the conclusion is clear: inventory overhang cannot be solved within silos. It requires ecosystem-level visibility and coordination.

Ecosystem Orchestration

Inventory build-up in aerospace is a structural byproduct of how the industry now designs, sources, and maintains aircraft. Reducing inventory alone will not solve this. The shift required is toward coordinated transparency across independent enterprises governed by compliance, traceability, and commercial discipline.

A tier-2 supplier holds certified excess material from a ramp-up phase.

An OEM faces an urgent configuration change.

An MRO carries elevated spare buffers due to turnaround delays.

In a siloed system, these remain disconnected.

In an orchestrated ecosystem, validated excess at one node becomes supply at another before it turns into stranded capital.

This is the direction Cnerzy is advancing toward: building structured digital infrastructure that enables cross-tier coordination and converts fragmented inventory into mobilized capacity.

From Risk to Resilience

The next competitive advantage of aerospace supply-chain leadership will not come from owning more stock, but from enabling the system to see, validate, and redeploy what already exists. The shift has begun.

Explore how ecosystem-based inventory orchestration can work within your supply network with Cnerzy.

Source

- McKinsey & Company – Supply Chain Risk, Resilience, and Rebalancing in Global Value Chains

- Gartner – Future of Supply Chain: Resilient and Agile by Design

- IDC – Future of Supply Chain

- MIT Center for Transportation & Logistics – Supply Chain Resilience

- Oliver Wyman – Global Fleet & MRO Forecast

- International Air Transport Association (IATA) – MRO Capacity Reports